As I was reviewing my notes while I was preparing to give a guest lecture at the MBA students of Haas School of Business, last December, I thought I would share some interesting data and personal insights about the Venture Capital industry.

Just to give you some background, these are personal notes I take as I study and research industry trends and novelties for my own curiosity. What I share in this post is in no way connected to my work at BootstrapLabs and in no way intended to suggest any particular investment opportunities.

My main reason for sharing these is to get your input, comments, and points of view on these topics – any comment or conversation this brings about is welcome and appreciated! Should this spark any discussions and conversations I was thinking of hosting a breakfast with other friends in the VC industry here in San Francisco this year. Please reach out if you would be interested in joining!

Although it has been a short six years that I have actually been working in the VC industry, it has been a long-time interest of mine and I’ve been tracking the growth and development of different firms for over fifteen years, some even from conception. Now more than ever, I track the industry daily and in detail as it is a space that is evolving rapidly and it is fascinating to see how the players are adapting their practices to keep up with what I like to call the VC revolution.

The future of this dynamic industry is up in the air but the upside of this big question mark is that there are many different trial and error practices being put in play by incredibly knowledgeable and admirable firms and it has been a whirlwind to observe the innovative methods growing out of the need to adapt to the changing climate and to combat the unknown.

———————–

While the performance of the Venture Capital industry is still on track to be one of the best in the financial assets class, long term successful firms are struggling, the level of noise for fund managers is at the every time high, micro-funds are thriving, and non-understandable maga fund (ex. Softbank) are messing up deals valuations!

Where we are today?

The always evolving economic landscape has finally pushed one of the more strategic economic financial asset class the “Venture Capital” industry to seeking for innovation, and consequentially started transforming.

Why is the VC industry so important?

0.24% of the GDP invested in VC, created 24% of the GDP in the US

What is changing the VC industry?

- Venture Capital firms are raising larger funds today.

- Venture Capitalists need to compete with multiple alternative forms of private capital at late stage.

- The market is more fragmented at seed stage; with crowdfunding, angels and micro funds playing a very important role.

- Liquidity takes longer (0 to IPOs is an over 10 years journey, and growing)

- Building ownership and access to deals is harder; Seed is the new series A.

- International competition on the rise.

- More capital raised by fewer startup deals.

In support of this analysis below you can find some of the trends I have been tracking over the last few months.

VCs AUM is skyrocketing

Growing at an unprecedented pace, total assets under management (AUM) reached a record $852bn as of September 2018.

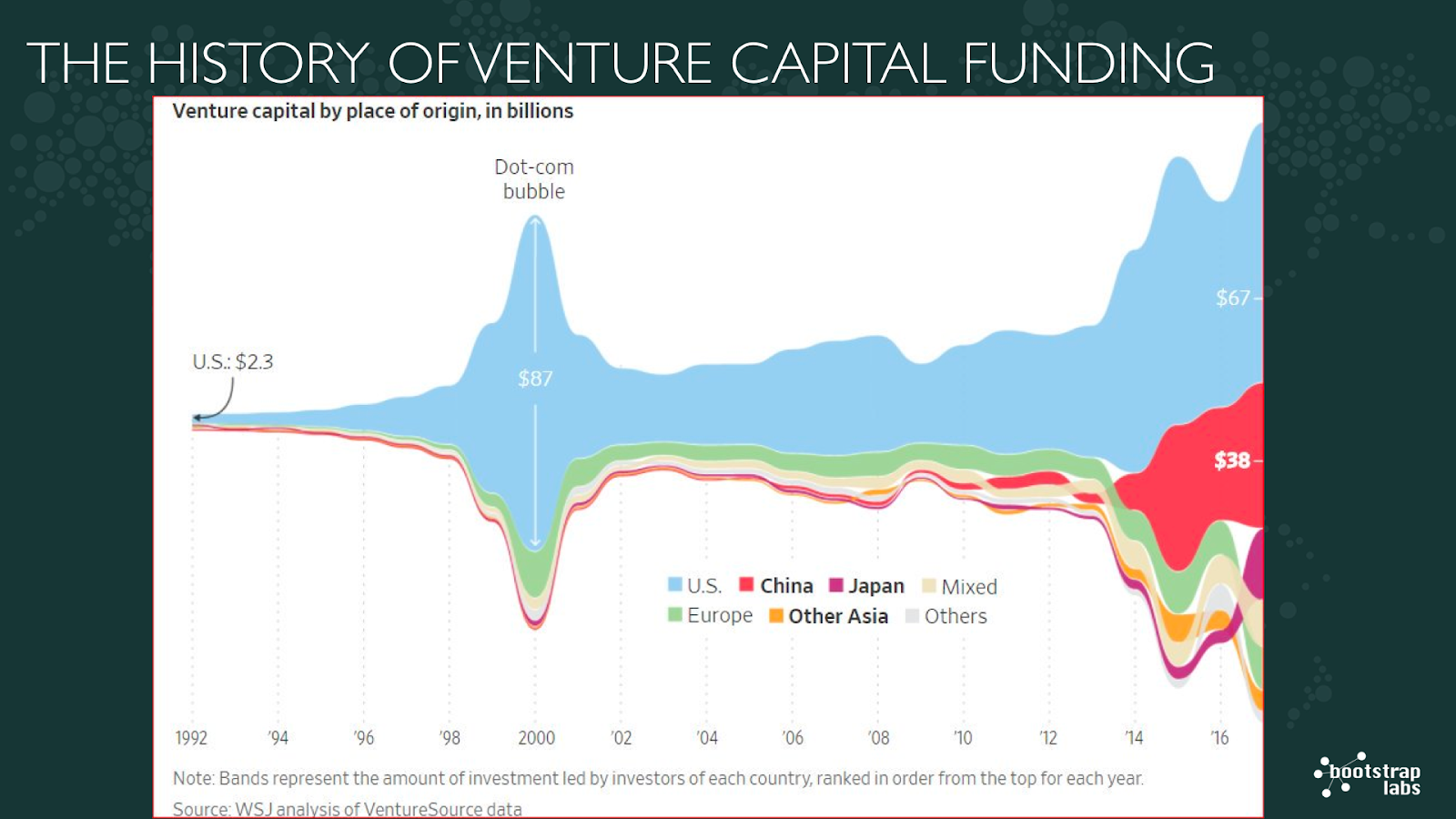

VC has evolved into a worldwide force

Asia-focused venture capital funds hold $334bn in AUM as of September 2018, up from just $75bn five years ago. Asia is significantly gaining ground on the US, which holds $397bn in AUM

US vs China

Further testament to the rise of the Chinese market, in 2018, the aggregate value of venture capital deals in Greater China ($107bn) surpassed US deals ($105bn).

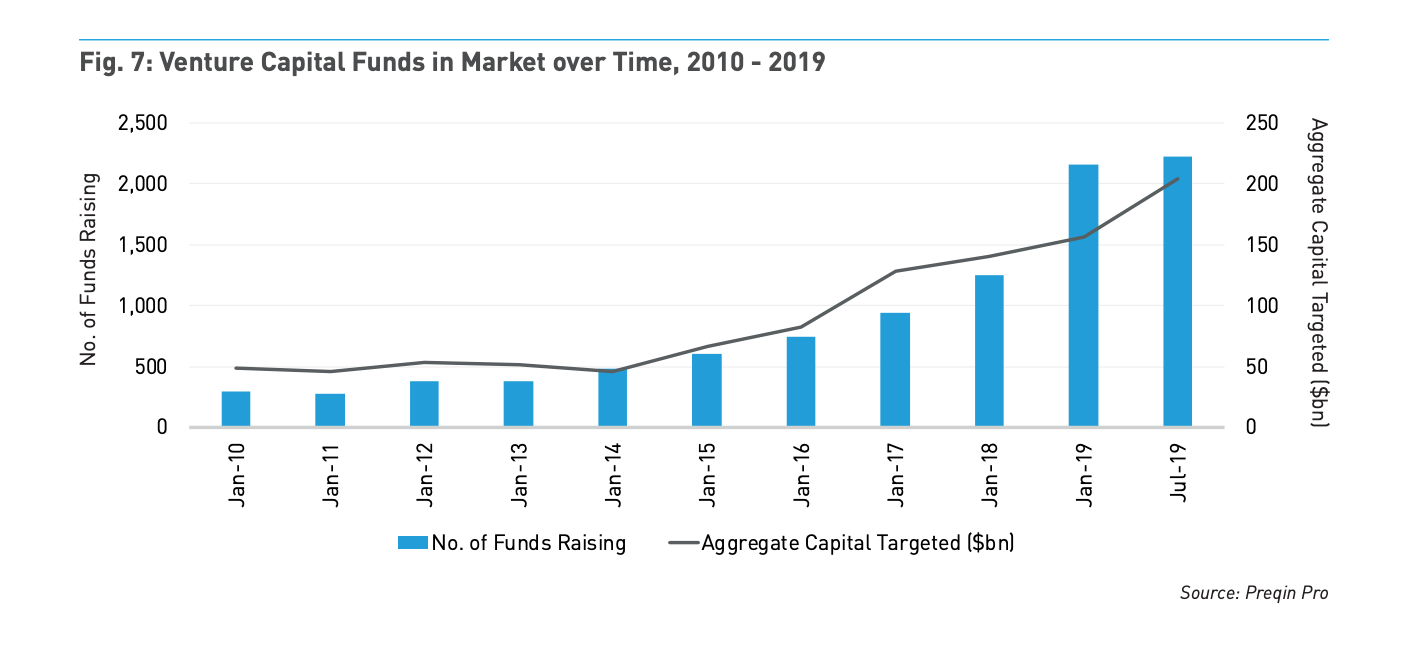

New funds keep on being raised

Annual aggregate capital raised has almost doubled in comparison with 2013, reaching $97bn in 2018.

Returns are still very strong:

Venture capital fund performance has been strong globally, and in 2017, a record $100bn in investor capital was called up.

VCs deals are getting larger

The average size of transactions in 2018 rose to $23mn from $6.7mn in 2013

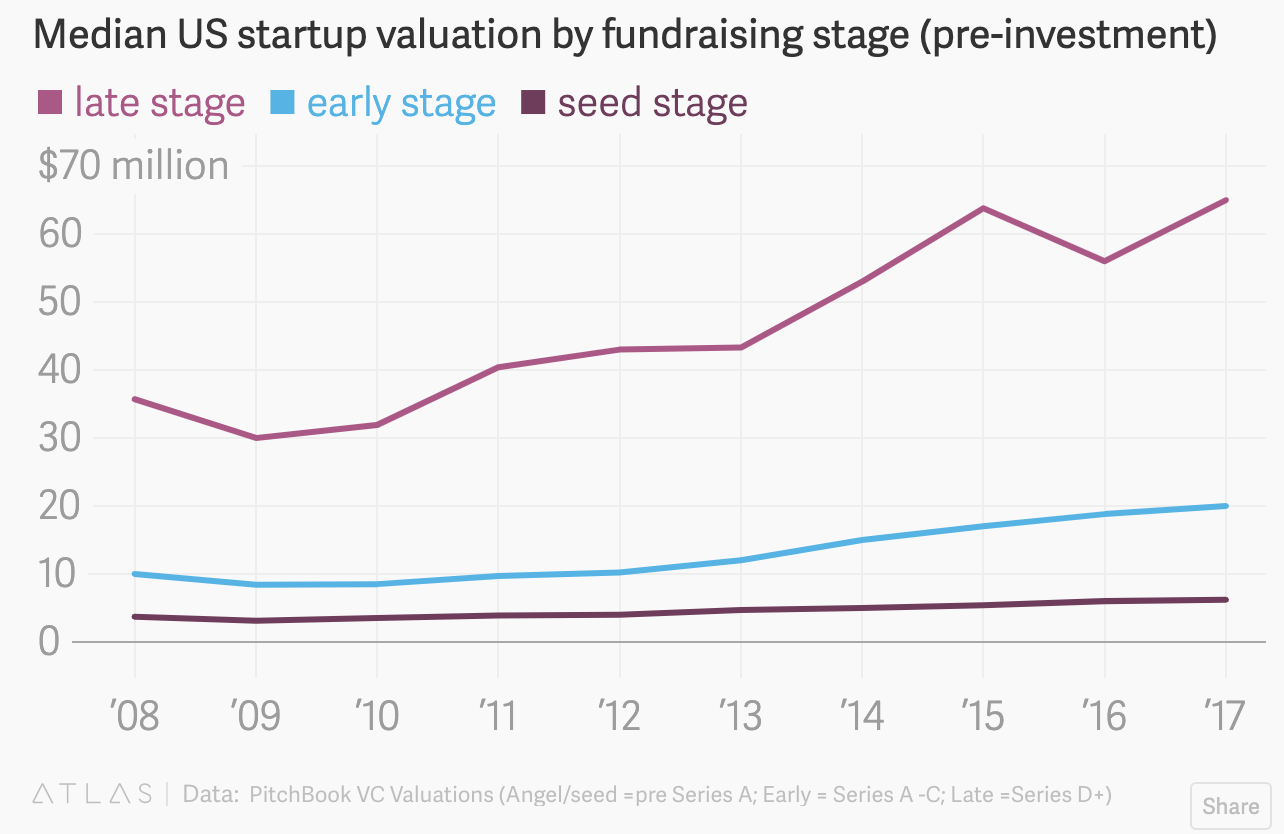

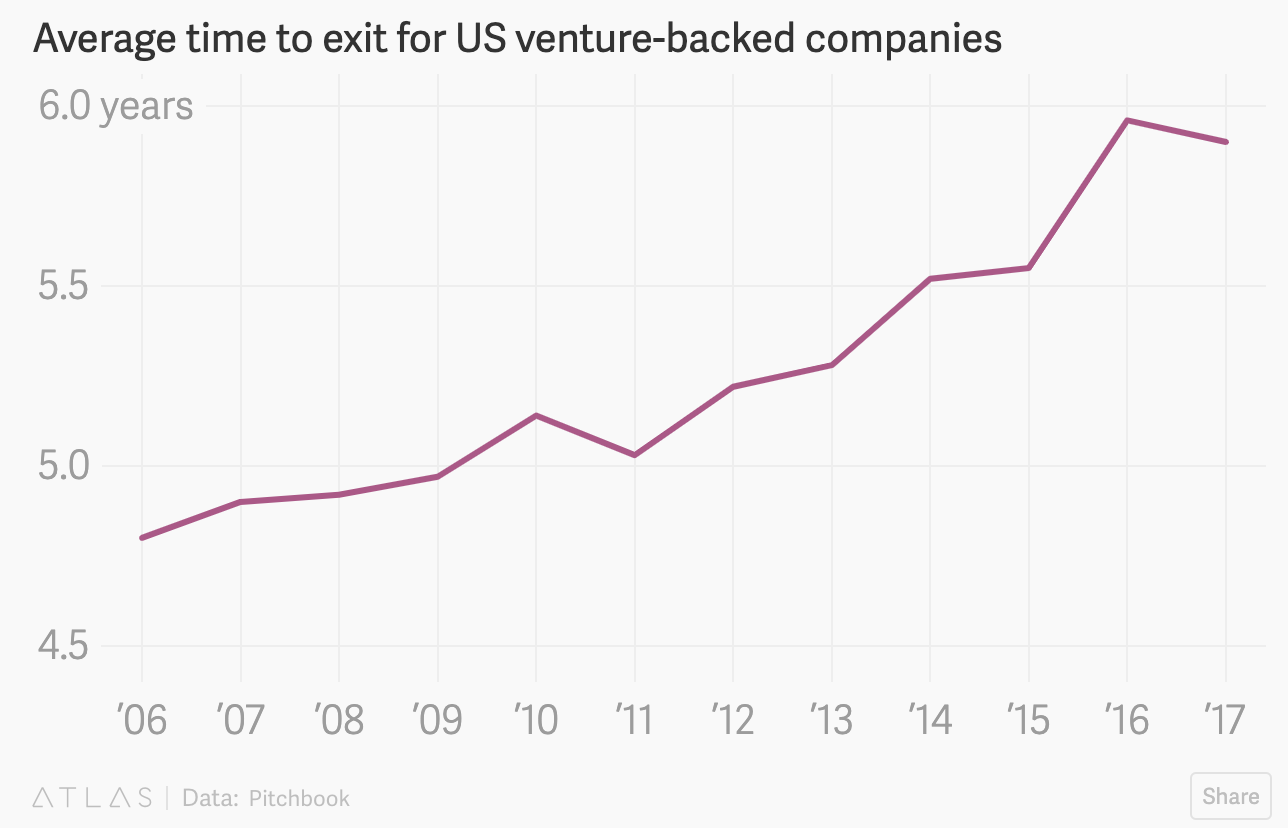

Startups valuations and average time to exit is growing

4x more VCs are now in the market

Number of funds in the market grove. Since 2014, the number of VCs in the market quadruplicate

US still the best market for exits but China is catching up

Exits in Greater China amounted to $41bn in 2018, which is less than half of the value of US exits, but represents over double the aggregate exit value in 2017 ($13bn).

Global exit value rose dramatically in 2018, reaching a record $170bn, in tandem with a decrease in the total number of exits between 2017 and 2018.

As mentioned, the US saw the most exits of any ecosystem, and at the highest total value ($88bn). At $30bn higher than the 2017 total, this was a record level for the region.

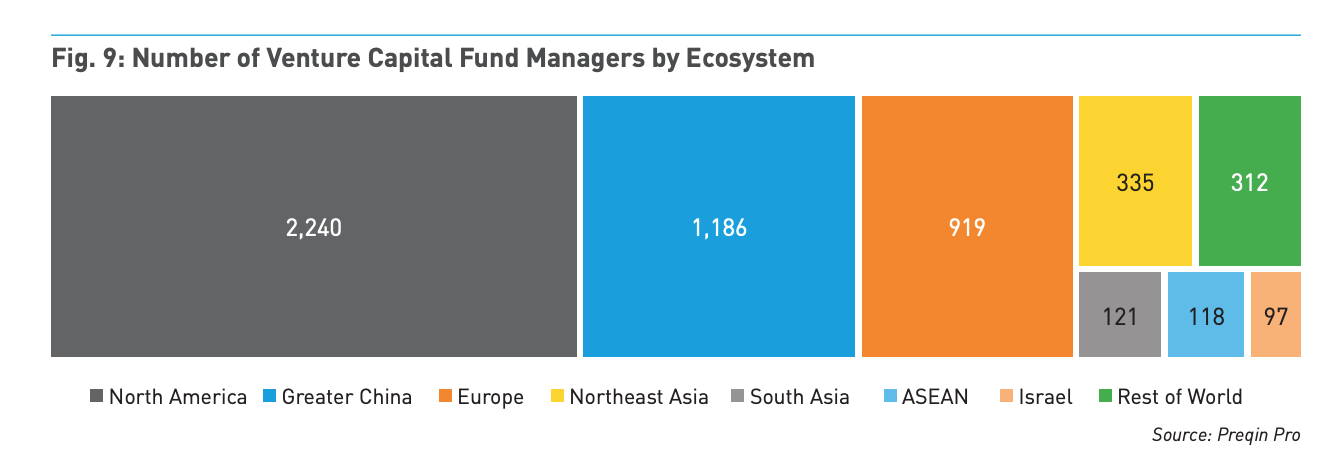

Number of funds managers

Historical Venture Capitals Allocation and Activity by Ecosystem

IPOs decline

Around 20 years ago we used to have 300 IPOs per year; today we see a little more than hundreds. Small-cap IPOs (>$50M) have declined faster than larger cap IPOs.

The 32 tech companies that went public in 2019 have only appreciated in value by an average of about 5 percent, according to Renaissance Capital, which tracks IPO performance. (September 2019). In 2018, that stat was about 13 percent. And in 2017? A 94 percent return rate.

Mutual Funds are much bigger today

From 1990 to 2000 the total asset under management reached $3.4 trillion; in 2016 was estimated to be around $16 trillion, a 5x growth.

Alternative private financing is on the raise

Startups stay private longer today. The time to go from first funding to IPOs used to be 6 years; today is over 11 years. The landscape of private investors who are betting on private companies at late stage has increased and includes today mutual funds, hedge funds, private equity buyout, sovereign funds, family office and more.

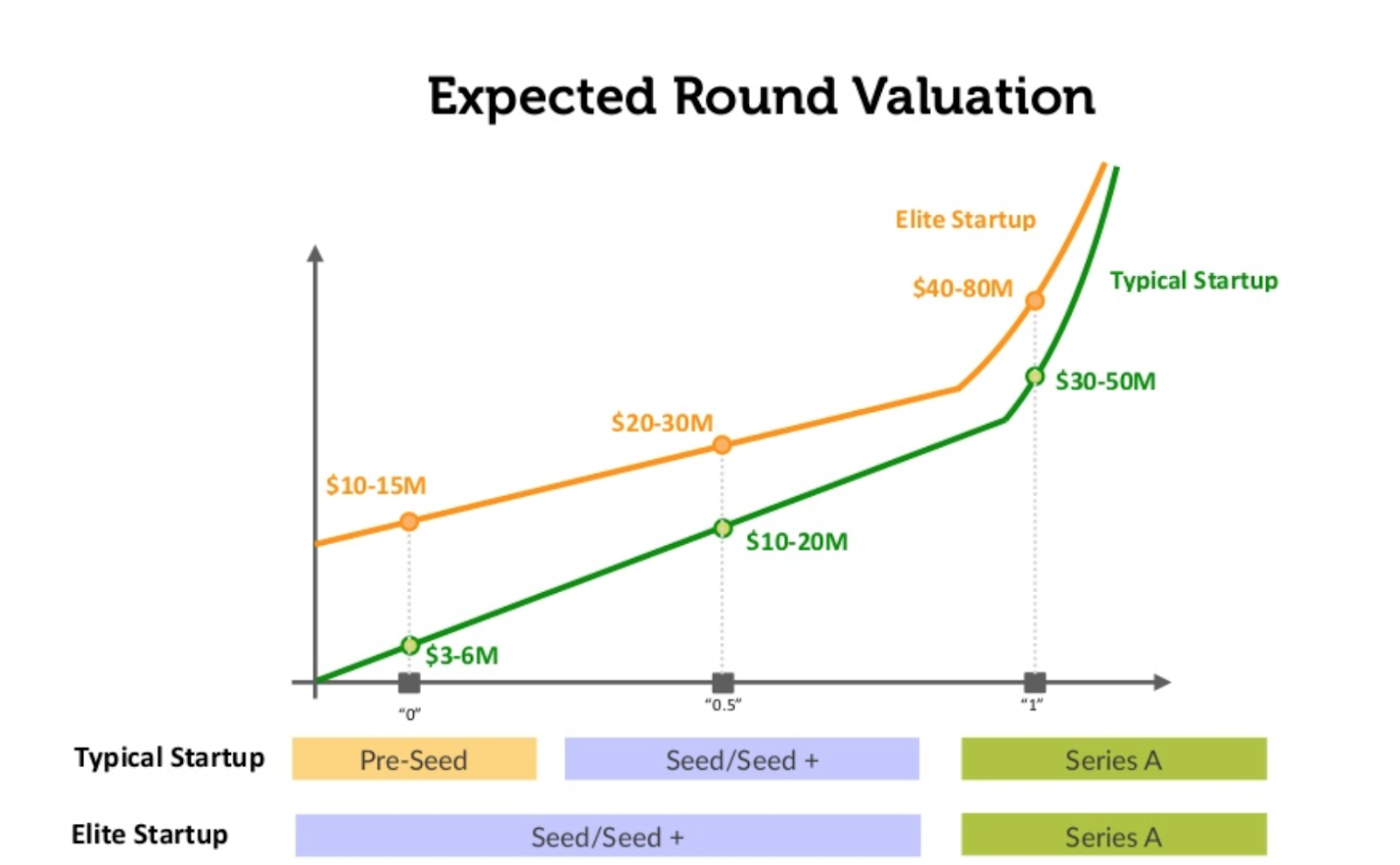

Average Valuation by round

—-

Sources: Many of the data points come from articles, pitchbook, cb insights, perquin and others.